The recent weeks and months have certainly been eventful, with the British public witnessing a new head of state, a new government, and an increasingly worrying economic environment. To add further volatility and uncertainty into the pot, Kwasi Kwarteng – the latest Chancellor of the Exchequer – announced a not so ‘mini’ budget on Friday the 23rd of September. In many ways, the budget went further than many expected, with wholesale reductions in tax and politically contentious changes to IR35 rules and the banker bonus cap.

Whilst it is not the place for Landlord Insider to pass judgement on the political policies of the day, the announcements made will have significant direct and indirect implications for landlords and property investors throughout the United Kingdom. As such, it is worth delving into what changes have been announced and what the implications are for landlords. These changes include:

- The announced amendments to Stamp Duty thresholds.

- The removal of the bankers bonus cap.

- The introduction an energy price cap until 2024.

- The reduction of income and national insurance tax.

Whilst individually, each of the above will have varying effects on landlords and the private rental sector, their aggregate effect on the economy and interest rates could well be substantial. It is certainly worth considering what these announcements may mean for property prices and mortgage rates over the coming years.

Amendments to Stamp Duty Thresholds

One of the most obviously property related proposals announced by Kwasi Kwarteng are the intended changes to Stamp Duty. As of the 23rd of September, the government have amended the thresholds and rates at which property buyers are required to pay Stamp Duty, benefiting both experienced buyers and first time buyers alike. The changes announced are as follows:

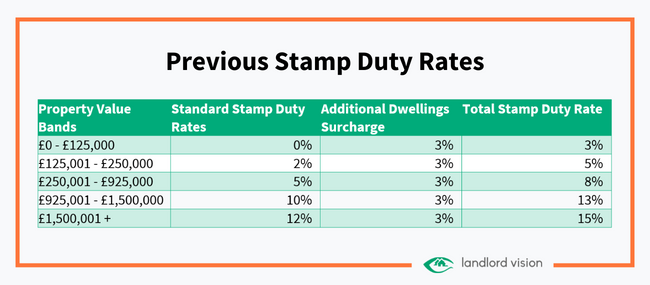

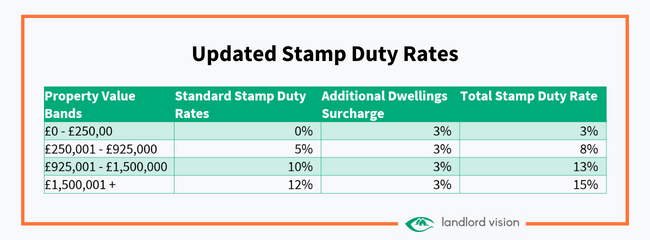

- The threshold at which house buyers begin paying Stamp Duty has been increased from £125,000 to £250,000.

- The threshold at which first-time buyers start paying Stamp Duty has been increased from £300,000 to £425,000.

Stamp Duty Land Tax (SDLT) is applied whenever you purchase a house in England or Northern Ireland. The rates paid depend on the overall value of the property being purchased, with house prices over certain thresholds accruing higher rates. There is a fair argument to be made that Stamp Duty is a regressive and economically damaging tax, so the announced changes are positive for landlords, homeowners, and the property market in general.

An update to Stamp Duty thresholds has been a long time coming. Forgetting for a moment the recent Stamp Duty holiday during the pandemic, rates were last updated in 2014, when the average house price was a mere £191,000. Since then, the average house price in the UK has risen to more than £256,000, whilst the stamp duty threshold has remained stubbornly fixed. If the threshold had kept pace with house price inflation, it would have risen to more than £167,500. The government estimates that by increasing the threshold at which home buyers begin paying stamp duty to £250,000, it will encourage an additional 29,000 property transactions each year whilst supporting those who can least afford to move home.

So, what does this mean for landlords? Firstly, the changes only affect landlords in England and Northern Ireland. Scotland and Wales have their own devolved versions of Stamp Duty (the rates and bands of which have been included at the end of this article). Secondly, landlords will still be required to pay the additional dwellings surcharge of 3% of the value of all properties, irrespective of their value. However, landlords will benefit from the overall increase in the zero-band rate, saving as much as £2,500 in Stamp Duty on each purchase. This can be seen in the two examples below:

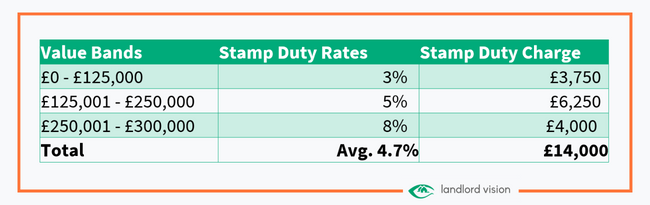

Example 1: Purchasing a £300,000 property before the announcement

Let us assume for a moment that a landlord went out and purchased a buy-to-let property for £300,000 prior to the announced changes. They would be required to pay 3% of additional dwellings surcharge on the value of the property up to £125,000. Then a further 5% of Stamp Duty on the next £125,000. Finally, they would need to pay a rate of 8% on the final £50,000 of the purchase price. All in all, the landlord would need to pay a total of £14,000 in Stamp Duty, equivalent to an average rate of 4.7% on a £300,000 purchase.

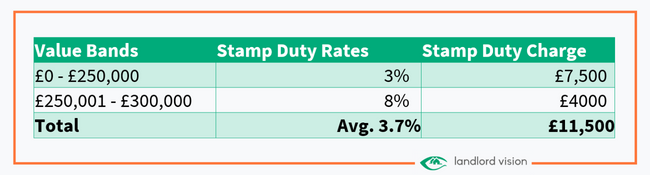

Example 2: Purchasing a £300,000 property after the announcement

Now let us assume that a landlord goes out and purchases a property after the 23rd of September for the same price of £300,000. As the thresholds have been increased, the landlord will only pay the 3% additional dwelling surcharge on the first £250,000 of the property’s value, with a further 8% charge levied on the remaining £50,000. Therefore, in total, the landlord will pay £11,500 in Stamp Duty on the property, equivalent to an average rate of 3.7%. This is £2,500 less than in the first example, prior to the announced changes.

Removal of the Bankers’ Bonus Cap

One of the most politically contentious announcements has been the intention to scrap the Bankers Bonus Cap, which was introduced by the European Union following the last financial crisis. The legislation prevents European and, until recently, British banks from paying employees bonuses that are more than 100% of their basic salary, or 200% in select cases. You may at this point be wondering what on earth this has to do with landlords and the private rental sector. The answer is that removing the cap will be a boon to the financial services industry and property/rental prices in London.

London is one of the pre-eminent financial centers of the world. The capital competes with the likes of New York, Hong Kong, Paris, and Frankfurt to attract the best talent, in the pursuit of influencing global financial markets. Without delving too much into the mechanics of the Bankers Bonus Cap, its removal will help to make the financial services sector, which accounts for 8.4% of UK GDP, more competitive on the world stage. Foreign banks will be more likely to base high-paid employees in London than Paris or Frankfurt. Top earners will no longer see New York as the go-to location if they want to earn the highest compensation. In short, London is likely set to see an influx of higher-paid workers and all the ancillary headcount and support services that their work will require.

In theory, aside from making UK financial services more competitive, the announced removal of the Bankers Bonus Cap will help to support house prices in and around London – where over half of the UK’s financial services GDP is generated. There will be increased demand for high specification properties in and around the City of London and desirable commuter locations. Whilst it is hard to quantify the exact scale of the changes this announcement will bring, it is certainly a positive one for landlords in and around London.

Energy Prices Capped Until 2024

Although it was announced ahead of the ‘Mini-Budget’ one of the most significant announcements for landlords is without doubt the decision to cap energy prices at an average price of £2,500 until 2024. The implications for tenants and landlords alike cannot be understated.

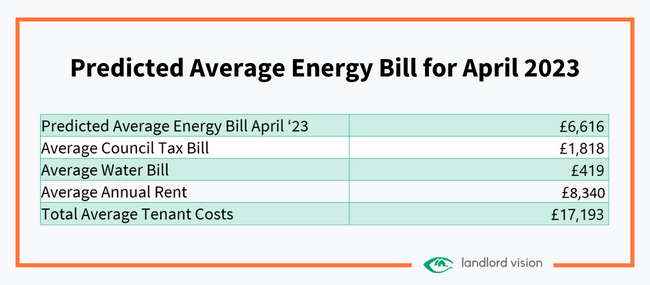

The war in Ukraine and the subsequent economic sanctions on Russia it has brought about has sent global energy markets into disarray. Energy prices have risen globally and especially so throughout Europe, as nations face restricted access to Russian LNG and Oil. It was predicted that household energy bills were set to rise to £3,549 in October, with further rises in January and April 2023 pushing bills as high as £6,616 a year. It is worth putting that into context. The median private rent in the United Kingdom is £695pcm or £8,340 per annum. Without the price cap, the average household would be facing £6,616 in energy bills, £1,818 in council tax, and £419 in water bills. Therefore, spending a total of £8,853 on energy, water, and council tax bills a year, £513 more than they would be paying on rent.

The median disposable household income (after taxes have been deducted) in 2020 was £29,900. Without the introduction of the energy price cap, the average household would have been left with just £1,058 per month in disposable income. It is likely that more than half the population would have even less than this per month to live off. Without the introduction of this policy, the situation for landlords and tenants alike would be bleak as the winter months set in. A significant proportion of tenants would have been unable to support paying both their energy bills and rent. Rental arrears would have risen, and an increasing number of tenancies would have been cut short. Demand for new tenancies would have likely begun to wane. Generally, the outlook for landlords and the private rental sector would have been devastating.

Whilst it is fair to argue the merits of different solutions and proposals. It should be acknowledged that the introduction of an average price cap of £2,500 until 2024 is far better than the prospect of no price cap. Certainly in the short term, it should be viewed as a positive announcement for tenants and landlords alike.

Reductions in Income Tax and National Insurance Contributions

Less directly linked to landlords and the private rental sector has been the government’s announcement to reverse the hike in National Insurance Contributions and cut the base rate of income tax from 20% to 19%. Fundamentally, irrespective of the relative tax cuts for high earners, these changes will have tangible benefits for the average earner. Reducing the basic rate of tax by one percentage point, to 19% will leave 31 million households across England, Wales, and Northern Ireland £170 better off on average. More importantly, the reversal of the 1.25% rise in national insurance, announced earlier this year, will benefit 28 million people across the UK to the tune of £330 on average.

Whilst we are not dealing with life changing numbers, the average household and tenants will be £500 better off due to the announced changes. This will provide homeowners and tenants with increased financial support as economic conditions worsen and recession looms. Although a small change, it will help to support average rents and reduce the likelihood of increased rental areas for landlords.

The Economic Impact of the Mini-Budget

The ‘Mini-Budget’ heralds a significant change. It introduces a raft of changes. The mantra, now more than ever, is about instilling and encouraging economic growth. Whether or not the policies will be successful in doing so is not the remit of this blog, but understanding the financial market implications is paramount to landlords.

Financial markets have not responded positively to the announced changes. Sterling dropped sharply during intra-day trading, with Gilts (UK government debt) spiking at the same time. Although it is worth pointing out that the fall in Sterling and rise in Gilt yields did not occur in isolation, with the Euro dropping heavily and other national government debt selling off in tandem. However, the most important thing for landlords to understand is what the market’s reaction suggests about interest rates and, thus, mortgage rates.

Financial markets are now pricing in the expectation that the Bank of England (BoE) will continue to raise interest rates this year, with markets predicting that the BoE will increase rates by 120 basis points. This is on top of the BoE’s 50bp hike (0.5% increase) on the 22nd of September, meaning rates could be as high as 3.45% as we enter 2023. Looking further ahead, markets expect rates to surpass 5.5% next year as the Bank of England seeks to combat double digit inflation and investors flee spiraling government spending.

This has huge implications for mortgage rates. Lenders usually price their mortgages at a premium over and above the BoE base rate. If the base rate reaches 5.5% next year, the increase will be directly passed onto borrowing costs. This poses two challenges for landlords. Firstly, the cost of financing new properties will be significantly greater, eating away at the return landlords can achieve. Secondly, it poses the question of affordability. How many landlords and homeowners on variable rates can afford to service their mortgage payments should mortgage rates reach 8.5%? Should enough homeowners and landlords come to the conclusion that paying such rates is unsustainable, then we may well see a wholesale sell-off in the housing market and a corresponding reduction in house prices across the board.

It is worth caveating that the future is not inevitable and this is merely what the financial markets are currently predicting. It may well come to pass that rates do not rise as high as predicted and homeowners cope with higher energy bills and mortgage payments. But landlords would do well to have sufficient cash reserves put aside in case of a rainy day. Certainly, the forecast remains troubling.

Appendix: Scottish Land and Buildings Transaction Tax (LBTT) and Welsh Land Transaction Tax (LTT)

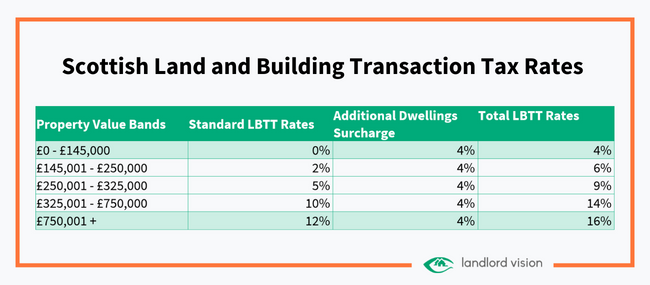

As mentioned above, the changes announced only affect landlords and home buyers in England and Northern Ireland. Landlords in Scotland and Wales face different rates and bands when purchasing properties. Landlords in Scotland are required to pay the Land and Buildings Transaction Tax (LBTT) when purchasing a property. Landlords are required to pay a 4% surcharge to the LBTT when buying an additional dwelling, with an example of the rates and thresholds included below:

Welsh landlords and homeowners face a separate set of rates and thresholds for properties located in Wales. However, much like Scotland, England and Northern Ireland, landlords are still expected to pay higher residential rates when purchasing additional dwellings. A breakdown of the thresholds and rates can be found below: