Conveyancing is the process of preparing and compiling legal documents for a property transaction. It is a necessary requirement for purchasing, selling and remortgaging a property. If a lender is involved in the process, which they often are, they will stipulate that a professional conveyancer or solicitor is used as part of their mortgage offer.

For many buyers, conveyancing can be a confusing and frustrating process. Any seasoned landlord will tell you that the process can be rife with delays and legal jargon. However, a basic understanding can help reduce stress and expedite the process.

Instructing A Conveyancer

The first step is determining who will be undertaking the conveyancing work. Whilst some experienced cash buyers may wish to act as their own conveyancer, most investors and landlords will choose to instruct a conveyancer. This means you will have to source and pay for the appropriate legal services.

There are two possible approaches. Investors can engage a trusted and experienced conveyancer early in the process, with some conveyancers acting on a no-sale, no-fee basis. Having a trusted conveyancer can be a valuable source of advice and provide a degree of confidence in how the process will proceed. The other option is to choose a conveyancer once you have determined the most economical lender. Choosing this route can potentially save costs.

Conveyancing fees can be split into two main categories:

- The legal fees paid to the conveyancer for preparing legal documents and providing legal advice.

- The disbursements paid to third parties for services such as searches or bank transfers.

Fees themselves will typically be around £850 to £2,000 depending on the firm and type of purchase. Leasehold properties and limited company purchases can result in higher fees.

Leaseholds require additional documentation such as a Deed of Covenants, which outlines the responsibilities of buyers and management companies. They can also require additional investigation into the length and terms of the lease. All of which can contribute to leaseholds incurring higher conveyancing costs.

Purchasing Through A Limited Company

As is increasingly the case, many properties will be purchased through a limited company structure. Purchasing a property in this manner, whilst tax efficient, can add additional legal requirements and costs to the process. It can also add 3 to 6 weeks onto the conveyancing process.

Conveyancers will need to conduct limited company checks when a property is purchased through a company structure. All directors and shareholders with significant control (over 25%) will need to provide proof of identity. The conveyancer is required to confirm that the company is entitled to purchase the property. As such, they may request written confirmation that the company’s board agree that taking out a mortgage is consistent with the company’s Memorandum and Articles of Association. This will usually be in the form of a signed document detailing board minutes where the terms of the purchase are discussed.

Understandably, the additional checks and documents required for limited company purchases will incur additional costs. These can often be in the range of £200 to £300. On top of this, many lenders will specify that company directors personally guarantee any mortgage they take out. For the vast majority of cases, it will be a requirement that the directors seek independent legal advice (ILA) so that they fully understand the implications of their guarantee. Although, some lenders do allow written waivers instead of this. Independent legal advice can cost between £300 and £500, potentially multiplied by the number of directors. Consequently, limited company conveyancing will often cost £500 to £700 more overall, plus VAT.

What Is A Lenders Panel?

It is not only the buyer and the seller that require a conveyancer. Mortgage lenders also need to instruct conveyancers to ensure that the property meets their lending criteria. Often, it makes sense for the buyer’s conveyancer to also represent the mortgage lender. Such a decision can prevent delays and is an economical choice.

Every lender has their own set of specific requirements that a conveyancer must meet. Often, they will mandate that the conveyancers have three or more partners, or require that they be accredited by the Law Society’s Quality Conveyancing Scheme. As such, lenders will have a list of approved conveyancers whom they are willing to work with. This list is called the Lenders Panel.

There are hundreds of lenders, all with their own panels. Few, if any, conveyancers will be on every lenders panel. If a buyer wishes to proceed with a conveyancer who is not on the lenders panel, the buyer will be required to contract and pay for the work of another conveyancer to act on behalf of the lender. This can result in additional delays and costs.

How to Pick the Right Conveyancer

Picking the right conveyancer is vital. Landlords and investors may be tempted to choose the cheapest possible option. Whilst this is understandable, landlords that choose this route may live to regret it. According to the legal ombudsman, a quarter of all complaints in 2016 were in relation to conveyancing work. Whilst there may be affordable deals out there, be prepared that the price paid may be in time rather than currency. A few hundred pounds may seem less valuable after months of chasing your conveyancer.

What steps can you take to pick the right conveyancer? Firstly, if you are using a lender, you will want to ensure your conveyancer is on the lenders panel. If they are not, you will need to be comfortable with paying additional fees.

It goes without saying that the price will be a consideration and it is worth getting a number of different quotes to check the lay of the market. However, it is also important to clarify who will be representing you from the conveyancer. Often it will be junior members of the firm that will be your main point of contact. Larger firms can often experience a higher turnover of such staff and you can face the frustrating predicament of your case handler leaving the firm midway through the process.

If purchasing a property through a limited company, you will want to check that the conveyancer is experienced in dealing with limited company purchases. Equally, if the property you are purchasing deviates from the standard run of the mill terrace or detached house, it may be worth ensuring that your conveyancer is capable of dealing with more specialist processes.

As is the case with tradesman, one of the best routes to a good conveyancer is through recommendation. Check online reviews and message boards. If using an independent mortgage broker, ask for their recommendation as they will have untold experience in dealing with conveyancers. However, be aware that some parties, especially sales agents, may receive commission for recommending certain conveyancers.

Building Insurance must Meet Lender’s Criteria

In nearly all cases, building insurance will be a mandatory requirement by the mortgage lender. As a minimum, the insurance will need to be sufficient to cover the outstanding mortgage. However, often lenders request that the insurance covers the minimum reinstatement value of the property. That is, how much it would cost to entirely rebuild the property.

Buyers can choose a building insurance policy which suits their needs, so long as it also meets the lenders requirements. The lender may ask for evidence that they are a named party on the insurance. Evidence of the policy being in place will need to be provided before contracts are exchanged.

Initial Queries – First Steps When Engaging a Conveyancer

Once a conveyancer is engaged, their first action will be to review the draft contract. Initial queries and routine questions will be raised to the seller to confirm basic details about the property. The conveyancer will also check to determine whether the property is freehold or leasehold. If it is leasehold, they will seek clarification about the length of the lease. The conveyancer will also instruct searches on the property.

What are Property Searches

Searches are conducted during the conveyancing process as a form of due diligence. The searches will take the form of a number of legal checks, either recommended by the solicitor or required by the lender. Searches include:

1. Local Authority Searches

A local authority search will comprise two parts, a LLC1 and a CON29. The Local Land Charges Register Search (LLC1) will consider factors such as whether the property is located in a conservation area, whether it is a listed building and whether there are any approved or conditional planning permissions in relation to the property. CON29 will query any planning permissions in the surrounding area which might affect the property and proposals for new roads and railways nearby.

2. Chancel Repair Queries

A quirk of British law is that some properties can be liable to pay for church repairs. This liability can date back hundreds of years. Properties effected by this may need to take out chancelry repair insurance.

3. Reviewing the Title Plan

Conveyancers will review the title plan to confirm that the seller owns the property that they are selling. The Land Registry will also confirm any terms of ownership and additional property related information.

4. Environmental Search

One of the most common searches, environmental searches are usually conducted by either Groundsure or Landmark. The report details a range of potential risks and hazards including flood risks, contaminated land, radon gas, landfill sites and potential ground stability issues.

5. Assessing the Flood Risk

The Land Registry can provide maps highlighting local bodies of water within 250 metres of the property. The maps will detail to what degree the property is at risk of flooding. Often, flood risk reports are included as part of an environmental search.

6. Water Authority Checks

Searches might check how water is sourced to the property and whether any public drains may impact future extensions or building works.

7. Optional Location Specific Searches

Depending on the location of the property, additional searches may be required. Areas with a history of mining, such as tin mining in Cornwall, might need additional mining related reports.

Signing Contracts

Once the initial queries and searches have been completed, it will be time to sign the contract. Before doing so, you will want to ensure that a completion date is set. The completion date can depend on a host of considerations, especially if a chain is involved. However, typically it may be set 1 to 4 weeks after the exchange of contracts.

At this point, buyers will need to make arrangements for a deposit to be paid into the conveyancer’s account. In most cases, the deposit will be 10% of the property’s value. Whilst the actual figure transferred can be negotiated, you will always be liable to pay the full 10% should the purchase fall through.

It is at this point that many buyers will wish to attend the property again to ensure that all the fixtures and fittings are as originally expected.

Exchanging Contracts

Prior to completion, a time and date will be arranged to exchange contracts. At the time of exchange, the buyers and sellers’ conveyancers will ensure that both parties signed contracts are identical. When this has been confirmed, each signed contract will immediately be posted to the other party.

Once the contracts have been exchanged, you will be legally contracted to purchasing the property on a given date. Should you fail to do so, your deposit will be forfeit. Equally, the seller will be legally obligated to sell to you and will be unable to accept other offers on the property.

Contract Completion

As completion nears, the conveyancer will send a statement detailing the final amount payable to the seller. This will need to be cleared and held in the solicitor’s bank account a minimum of one day prior to completion. In addition to this, the conveyancer will formally submit an application to the Land Registry. The application will highlight your interest in purchasing the property and request that the deeds be frozen for a period of 30 working days.

A specified time will be set on the completion day. At which point, providing that the seller has received the necessary funds, the keys will be deposited at the estate agents for collection by the buyer.

After the completion date, the conveyancer will complete any outstanding requirements, such as paying any applicable Stamp Duty on your behalf and sending a copy of the title deeds to the lender. Your legal documents will be submitted to the Land Registry and you should receive a copy of them within 4 weeks. At this point, the conveyancing process has been completed.

How Long Does the Conveyancing Process Take?

Conveyancing can be a notoriously time-consuming process. This is one of the reasons why choosing a trusted and experienced conveyancer is so important. As a rough rule of thumb, the conveyancing process can take between 3 and 4 months. Cash buyers can expect a quicker process, whilst those purchasing through a limited company may experience a timeline closer to 4 to 5 months.

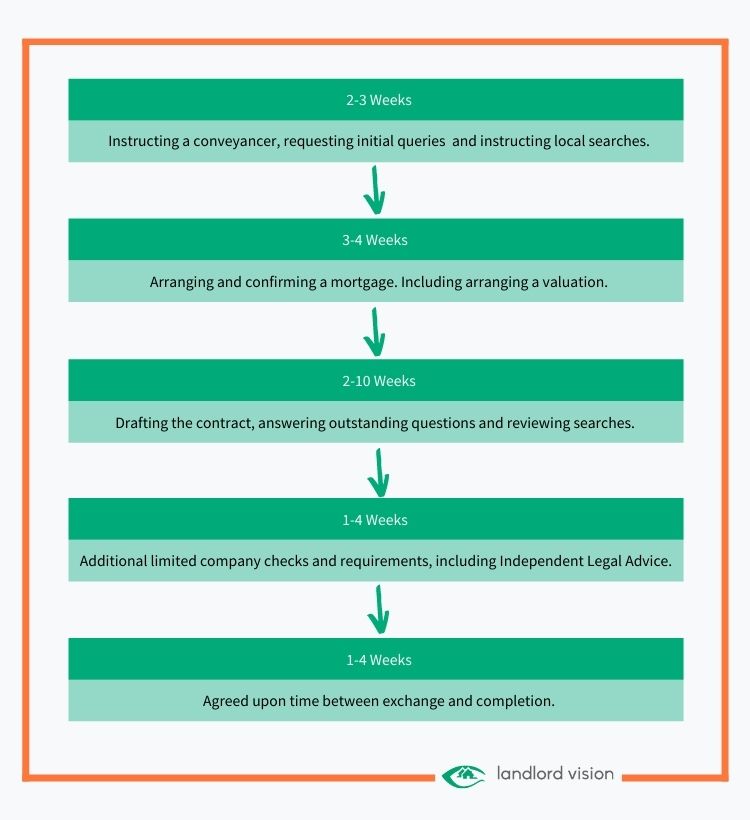

Whilst timelines can vary considerably, you can find a rough breakdown of each stage below:

Is There Anything you can do to Expedite the Conveyancing Process?

It is usually in everybody’s interest that the conveyancing process is completed as quickly and efficiently as possible. Whilst there may always be certain issues which arise that delay the conveyancing process, there are some things which buyers can do to expedite the purchase:

Firstly, buyers can ensure that they instruct both their conveyancer and lender as early in the process as possible.

- As a buyer, ensure that you have all your documentation prepared and to hand.

- Where possible, provide scanned and emailed copies of documents to your conveyancer. If you must send a document by post, ensure that it is sent first class.

- Ensure that you check, complete and sign all documents and actions as efficiently as possible. Responding quickly and efficiently puts the onus on the conveyancer.

- When you do communicate with conveyancers, ensure there is a written audit trail of your communications to refer back to.

- If you are experiencing delays on the conveyancing side without good reason, be a nuisance. Call up and ask to speak to your case handler on a regular basis. Always follow up with an email after a call.

- When you do write to or speak to your conveyancer, do so clearly. Always query what tasks are outstanding. If there is a hold up, ensure you understand what is causing it and request a plan of action to resolve the issue.

Disclaimer: This ‘Landlord Vision’ blog post is produced for general guidance only, and professional advice should be sought before any decision is made. Nothing in this post should be construed as the giving of advice. Individual circumstances can vary and therefore no responsibility can be accepted by the contributors or the publisher, Landlord Vision Ltd, for any action taken, or any decision made to refrain from action, by any readers of this post. All rights reserved. No part of this post may be reproduced or transmitted in any form or by any means. To the fullest extent permitted by law, the contributors and Landlord Vision do not accept liability for any direct, indirect, special, consequential or other losses or damages of whatsoever kind arising from using this post.