Whether it is in business or in life, the ability to manage one’s finances is a key requirement on the path to financial success. Landlords can appreciate this fact more than most. Regular mortgage payments and numerous expected and unexpected costs necessitate that landlords be on top of their cashflow. As such, it is important to ensure that you are using the right products and services to manage your finances. This entails everything from picking the right accountant, through to accessing the best software and bank account.

Why Do Landlords Need A Separate Bank Account?

Fundamentally, it is good practice to separate your personal and business finances. There are far more advantages to doing so than not doing so. This is especially the case when a property portfolio grows in size and scope.

If you are operating your properties through a limited company, you will need to use a business bank account, as the business is classed as a separate legal entity from the directors/owners. If you own your properties as a sole trader, you may be able to use your personal account in some cases. However, most personal accounts will have fine print which specifies that the account is not to be used for business purposes. Whilst some landlords operating a single property may be able to get away with using their personal account, the majority of landlords would be best advised to ensure they operate with a separate business bank account.

Using a business bank account is not just a necessary requirement. It can be an important step towards reducing the admin burden of operating a buy-to-let business. Separating business and personal expenses will save both time and costs when completing tax returns. Equally, where landlords may still work a full or part time job, it can be important to separate different income streams. Fully separating your personal and business finances will make it easier to assess the profitability of your properties, helping to inform the decisions you make.

Business bank accounts can support the long-term success of a property business. When using a separate bank account, your limited company will start to build up a credit history. This can be used to access business loans, financing and credit cards which can benefit your business long into the future.

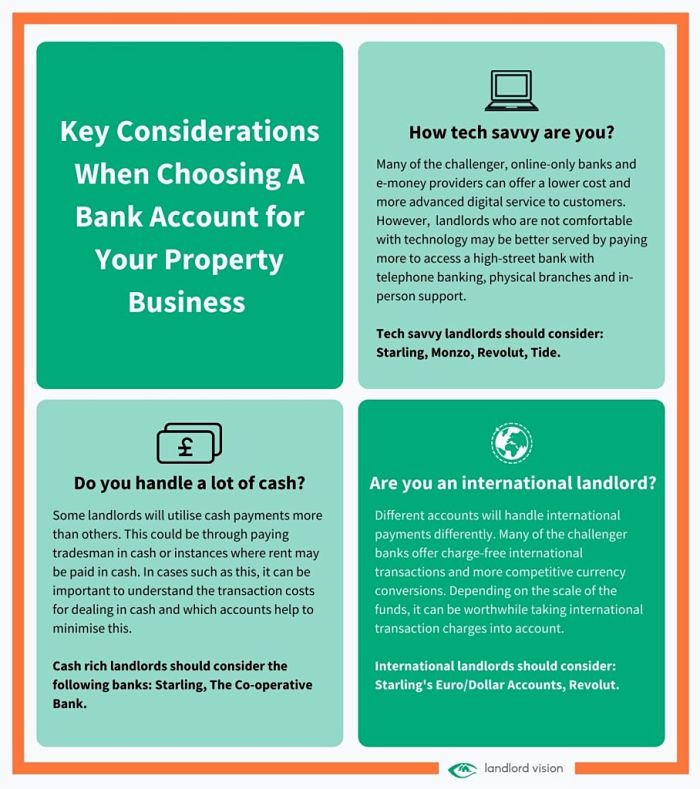

Key Considerations When Choosing A Bank Account for Your Property Business

There are a number of different factors which may be worth taking into consideration when choosing a business bank account. The importance of these factors will depend on the nature and scale of your property business:

- Monthly fees

- Transaction costs

- Payment restrictions

- Security and accessibility

- Ease of use

- Integration with other systems

The most profitable landlords are the ones who are able to most effectively minimise costs. Choosing the right business bank account can be an important step in ensuring that you are not paying over the odds for something that you don’t need.

Fees and Transaction Costs on Property Bank Accounts

Unlike personal accounts, many business bank accounts can come with monthly fees and additional transaction costs. The scale of these fees and costs can vary from one account to the next. It is important to choose an account which proves to be the most economical for the type of transactions that your properties will require. If cash plays an important role in your business, be it through paying tradesman or even the potential that rent is paid in cash, you will want to choose an account which facilitates this. Equally, international landlords may wish to choose an account which supports low-cost international payments.

Unique Requirements and Payment Restrictions on Property Bank Accounts

Property businesses can have unique requirements which may need to be considered when choosing a bank account. As such, it can be important to consider the payment restrictions associated with an account and whether they may prove to be a hinderance in the future. Some accounts can have transaction size limits or cap the amount you are able to pay or receive in a given day. For landlords operating on tight timelines or routinely engaging in large transactions, it can be worth considering the limitations placed on an account.

Security, Accessibility and Ease of Use for Your Property Bank Account

The next aspect to consider is the security and accessibility of your money. If you are planning on holding a large cash buffer in the account, it is important to ensure that the deposit is protected by the Financial Services Compensation Scheme (FSCS). Accounts registered under this scheme will have their deposits protected up to £85,000 should the bank fall into financial difficulty. Additionally, it is important to ensure that you have the means to readily access and use all the features of your bank. For traditional banks, this will involve checking whether or not a physical branch is located sufficiently close enough should you need it. For digital challenger banks, you will need to be comfortable using apps and online banking for all aspects of your current account experience.

Choosing a Property Bank Account That Integrates with Your Other Systems

The final aspect to consider is whether the bank fits with the software and services you already use. If you use an accounting package, it is worth checking whether the account is set up to connect to them. Landlord Vision customers may want to ensure that the account is enabled for Open Banking so that they can quickly and easily reconcile their transactions.

Changing Bank Accounts

You may be surprised just how easy it is to switch business bank accounts in 2022. Many of the banks in this article participate in the Current Account Switch Guarantee and provide support services to ensure that the transition is as smooth and hassle free as can be. Your new bank will ensure that any payments and direct debits are moved over to your new account. What is more, the guarantee means that on the off-chance that something does go wrong, the bank is required to reimburse you.

To change bank accounts, you will want to:

- Choose the new current account which suits you best.

- Apply for the account in question.

- Ensure your bank is using the Current Account Switch Guarantee.

- Choose a date when you want the switch to occur.

Irrespective of the bank or account that you opt for, the process will always be relatively similar. Money laundering regulations will require that you provide documentation detailing who you are and your business. Once this is done, your new bank will do all the heavy lifting for you, ensuring that your incoming and outgoing payments and current balance are carried across to your new account.

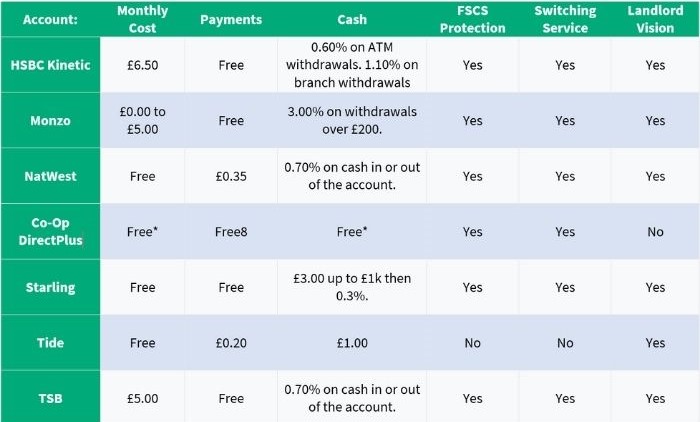

The Best Business Bank Accounts for Landlords in 2022

Starling Business Banking stands out from the crowd as the best overall bank for landlords. The bank was rightly awarded the Best British Bank award for the fourth consecutive year in 2021, also picking up awards for the Best Business Banking Provider, Best Banking App and Best Current Account. All of which come as no surprise, as it’s accounts combine easy to use functionality with some of the lowest usage and transaction costs on the market. Anecdotally, the bank is especially popular amongst landlords on forums and groups online, who often recommend the bank to their peers. For those willing to forsake the traditional high-street banks, Starling should certainly be on your list of options.

However, despite its standout credentials, Starling is not the only bank offering worthwhile services to landlords. To help you find the signal in the noise, Landlord Vision has compiled a list of the best business bank accounts for landlords in 2022. The list includes a varied mix of traditional high-street accounts, techy accounts from traditional banks and challenger online only banks to give you the best options in each case.

- Co-Operative Directplus

- HSBC Kinetic

- Monzo Business

- NatWest Business

- Starling Business Banking

- Tide

- TSB Business Plus

Finding the Best Bank Account for Your Properties

Admittedly, the world of challenger banks and online only options may not be to everyone’s taste. For landlords that may prefer sticking with a more traditional banking option, it may be worth considering either the TSB Business Plus Account or the NatWest Business Current Account. Smaller landlords will find NatWest to be a preferable option as the account comes with no monthly cost and free basic accounting software. In comparison, more established landlords may prefer the TSB Business Plus Account, which has no monthly charges if you have an average balance greater than £10,000 (£5pcm if not) and slightly lower transaction costs.

Savvy landlords willing to shop around may be enticed by the Co-Operative Bank’s attractive switch rates on their Business DirectPlus account. As of January 2022, new customers will benefit from a phenomenal 30 months of free everyday banking, with no maintenance or transaction fees. Although landlords that opt for this course need to be aware that charges will rise at the end of the initial 30 month period and that they required to ensure their balance does not fall below £1,000.

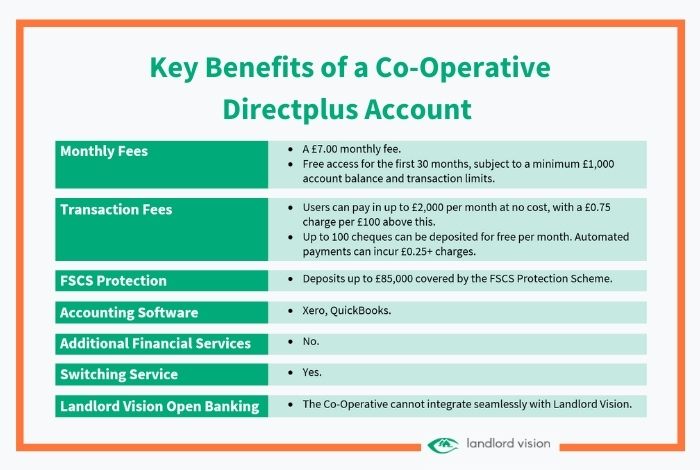

The Co-Operative Directplus Account

For the second year running, the Co-Operative bank has stood out as offering one of the most enticing banking deals to savvy shoppers. Their DirectPlus account provides customers with 30 months of fee free banking so long as they maintain a balance of more than £1,000. The offer makes the account one of the most affordable high street bank accounts available to landlords, combining mobile banking, branch banking and additional borrowing and saving features.

It is worth considering the limitations that come with the account. Firstly, once the initial period ends your tariff will rise to include a £7.00 per month maintenance charge and transaction costs of £0.35 for automated payments. Although the account does include up to £2,000 of fee free cash deposits and withdrawals. Secondly, the online and mobile banking functionalities may not be as seamless as some of the new challenger banks.

Key benefits include:

- Market leading introductory offer

- £2,000 of fee free cash withdrawals and deposits

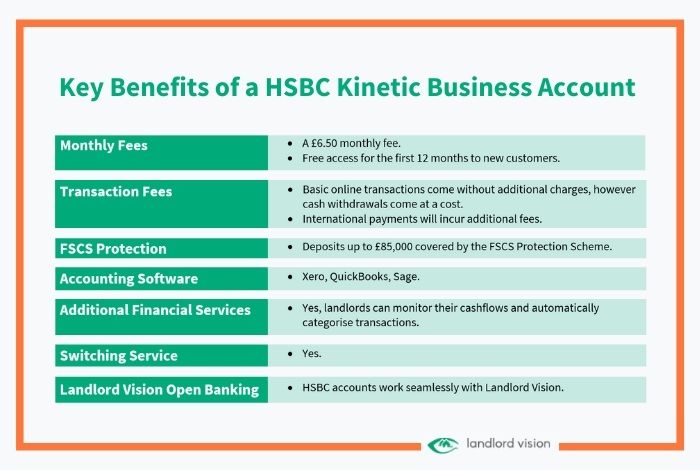

HSBC Kinetic Business Account

HSBC used feedback from 3,000 UK SMEs to develop the Kinetic Account. The account is their response to smaller digital competitors such as Starling. It aims to combine the financial and physical clout of HSBC with the technological benefits of app-based banking.

The Kinetic account can be opened digitally through the app and has been designed to provide in-depth insights and support to SMEs. Landlords will be able to better understand their cashflow, automatically categorise expenses and see account insights in line with HMRC tax coding.

Over the past 12 months, the account has added a number of new features, allowing landlords to access savings accounts, apply for overdrafts of up to £30,000 and make payments of up to £25,000 within the application. There is also an introductory offer, waiving maintenance fees for the first 12 months to new businesses and those looking to switch accounts.

Key benefits include:

- A quick and easy application

- The ability to see cashflow and spending insights

- Access to a linked savings account on application

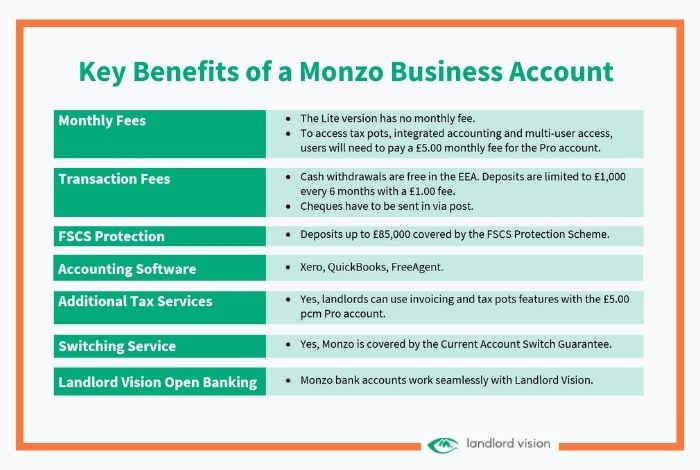

Monzo Business Account

Monzo business banking is open to UK based sole traders and limited companies. The bank provides online-only services to its customers. One of Monzo’s key selling points is its easy-to-use app which provides users the ability to set budgets and monitor spending more effectively. Landlords with smaller portfolios will be best suited by the Monzo Lite Account, which has no monthly cost. However, landlords with larger portfolios may prefer to opt for the Monzo Pro Account for just £5 per month, which includes additional tax and accounting features.

Tech savvy landlords will appreciate the quick setup, spending alerts and tax saving features. All of which can be used to help trim costs and increase profitability. However, landlords who operate with large cash transactions will be inhibited by the £1,000 limit on cash deposits over six months. Equally, any property business which is held in a partnership or less conventional structure will not be able to use Monzo.

Key benefits include:

- A simple and easy setup

- Spending alerts and in-app tax saving features

- Charge free spending, whether at home or abroad

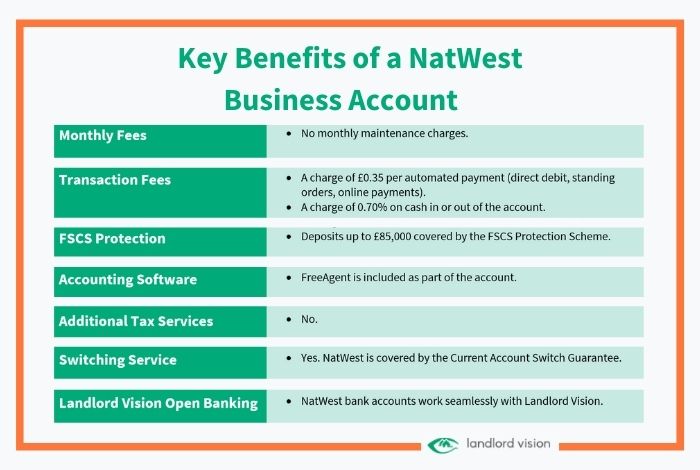

Nat West Business Account

The NatWest Business Account is one of the best traditional banking accounts available on the market in 2022. It combines relatively user friendly, mobile features with low costs and traditional branch access, making it one of the best all round accounts for landlords.

The account comes with no monthly maintenance charges, free accounting software and 24/7 Online, telephone and mobile app banking. Landlords will also be able to benefit from NatWest’s savings account and borrowing options, allowing you to keep all of your borrowing and accounts in one place. However, automated payments such as direct debits do incur a cost of £0.35 per item.

Key benefits include:

- No monthly maintenance costs

- Combining branch and app banking

- Free accounting software

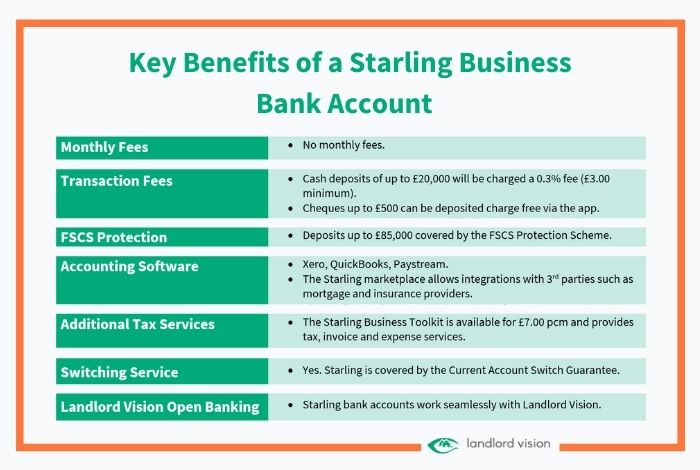

Starling Business Bank Account

Starling Bank is an online-only challenger bank operating in the UK. The bank has no physical branches and relies on its mobile application to provide full-service banking. Starling was voted the Best British Bank, Best Current Account Provider, Best Banking App and Best Business Banking Provider in 2021.

Starling operates both sole trader and business bank accounts. However, the sole trader account is only open to customers who already use a Starling personal account. Both accounts can be accessed with no monthly fees and no cash withdrawal fees from ATMs in the UK and abroad.

Anecdotally, Starling bank is a popular bank among landlords. The account offers an appealing combination of no monthly fees, reasonable transaction fees and a ready accessibility to online accountancy services. Equally, the banks FSCS protection makes it slightly more secure than some of the competing e-payment platforms.

Key benefits include:

- Relatively low costs compared to other accounts

- The Business Toolkit is a useful feature for landlords who do not already utilise accounting software

- A strong online offering at a time when more and more branches are closing down

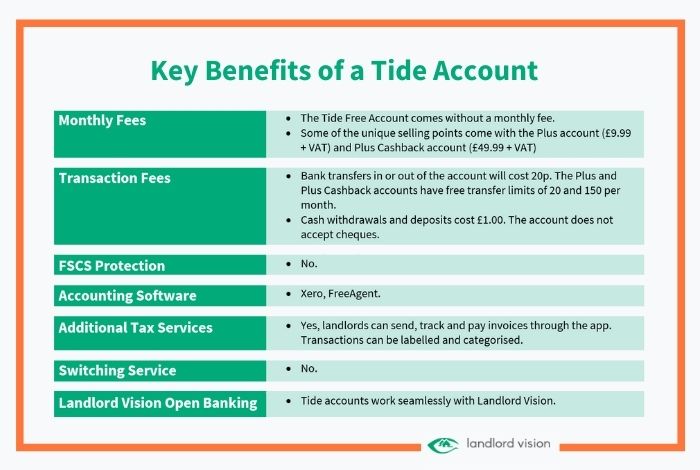

Tide Account

Aimed at small, tech-savvy business owners, an account with Tide can be set up in close to 10 minutes. Similar to its online-only peers, Tide aims to be easy to use and accessible anywhere. The account can be entirely managed through your smart phone.

Tide’s key selling point is its ease of set up. Customers can open an account digitally, without having to attend a branch in person. Customers are able to store and upload receipts from expenses which can then be categorised using the app. Additionally, landlords who may provide additional services on top of their lettings may find the free invoicing feature helpful.

One drawback is that Tide is not considered to be a bank. As such, it is not eligible for the FSCS scheme and deposits are not guaranteed by the government. That being said, the parent company of Tide (Prepay Technologies) states that it keeps an equivalent cash reserve for all deposits to protect them should Tide become insolvent.

Key benefits include:

- Quick account set up

- The ability to easily manage the account entirely through an app

- No monthly fees on the basic account

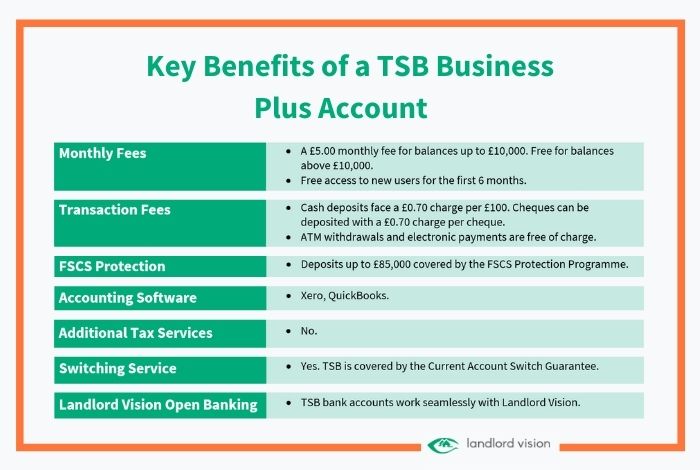

TSB Business Plus Account

Formerly part of Lloyds Banking Group and now owned by Spanish bank Sabadell, TSB offers a single business account to customers called the Business Plus Account. The bank offers the potential to earn one of the highest liquid interest rates on your cash balances through their associated savings account.

Landlords wanting access to more traditional banking will benefit from the ability to access 300 branches, online banking, mobile banking and telephone banking. Equally, landlords with large cash balances of more than £10,000 will be able to avoid the £5.00 monthly fees on the account, making it one of the more affordable high-street banking options.

Key benefits include:

- Access to a Business Instant Access Savings Account and earn a return of 0.30% AER on balances over £5,000

- Benefit from the ability to use 300 branches, online banking, mobile banking and telephone banking

Disclaimer: This Landlord Vision blog post is produced for general guidance only, and professional advice should be sought before any decision is made. Nothing in this post should be construed as the giving of advice. Individual circumstances can vary and therefore no responsibility can be accepted by the contributors or the publisher, Landlord Vision Ltd, for any action taken, or any decision made to refrain from action, by any readers of this post. All rights reserved. No part of this post may be reproduced or transmitted in any form or by any means. To the fullest extent permitted by law, the contributors and Landlord Vision do not accept liability for any direct, indirect, special, consequential or other losses or damages of whatsoever kind arising from using this post.