For many, a discussion on the intricacies and variations of UK tax policy might be compared to a form of long-lasting monotonous punishment. However, a recent London School of Economics (LSE) report commissioned by the National Residential Landlords Association (NRLA) draws some very interesting conclusions. The report compares the UK’s current tax regime with those found in comparable nations, such as France and the United States.

UK has Least Hospitable Tax Policies for Landlords in Europe

Interestingly, the report finds that landlords in the UK have a right to feel somewhat disgruntled by the current tax regime. The UK has one of the least hospitable tax policies for landlords in Europe, with individual landlords placed in a precarious position that defies the basic principles of taxing property. Whilst the UK hasn’t always been so inhospitable to landlords, the quantity and nature of recent regulatory changes have severely hampered the incentives of being a landlord.

The increased tax burden could be more palatable if it had occurred in isolation. Instead, higher taxes have come alongside greater regulatory requirements and generally unfavourable rhetoric from the government, as the LSE report highlights below:

“Individually and cumulatively, the recent changes have reduced the incentive to be a landlord. Landlords are observing the effects of higher taxes on returns, but taxation is not the only official lever: they also cite increasing regulation and bureaucracy and, importantly, the government’s negative messaging about private landlords and their role in the housing market.”

Scanlon, Whitehead and Blanc; London School of Economics.

Landlords are Economically Essential

Landlords play a vital and often underappreciated role in the UK economy, providing both temporary and long-term accommodation to the public. The properties which landlords maintain, and supply allow people to study and work across the UK, to quickly move closer to their loved-ones and to scale their living standards more rapidly. Yet, despite the private rental sector being broadly similar in size to the rest of Europe, UK landlords face a fare more punitive taxation regime.

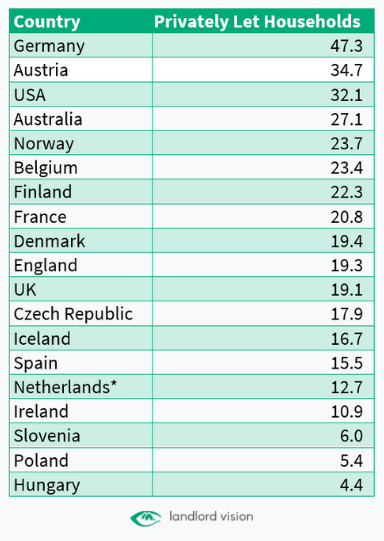

Comparing The Size of Private Rental Sectors Globally

Given the nature of housing debate and the manner in which the British media cover it, you might be forgiven for forgetting that the private rental sector is not a phenomenon unique to the UK. In fact, the scale of our domestic private rental sector isn’t far from the international average, with just less than one in five households residing in a rental property. Overall, 19.1% of households resided in privately rented properties in 2019, up from 16.4% of households in 2010.

UK’s Private Rental Sector Relatively Small

Broadly, the UK’s private rental sector is smaller than many developed western nations, with nearly half (47.3%) of German households renting from private landlords and close to a third of households in the USA (32.1%) doing the same. Interestingly, the size and scope of the UK’s rental sector compares closely to that of France, both in its current size (19.1% vs 20.8%) and in its growth since 2010 (UK: +17%, France: +18%).

Unsurprisingly, the private rental sector remains relatively small and formative in many former Eastern Bloc nations, such as Poland (5.4%) and Hungary (4.4%). However, the rental sectors in these nations are growing at a considerable rate, with the private rental sector in the Czech Republic growing by 231% between 2010 and 2019.

Overall, the data compiled by the London School of Economics suggests that the UK has a somewhat typical proportion of private landlords offering accommodation. A full list of the comparable rental sectors across 19 countries has been included below:

Proportion of households residing in privately rented properties (2019):

*Reconciling and comparing international data can be difficult. The Netherlands provide data detailing the housing stock owned by ‘other’ landlords. Other government statistics suggest that the private rental sector is closer to 28% in areas such as Amsterdam.

Changes In the UK’s Taxation of Landlords

Over the past 6 years, the government have introduced a succession of punitive changes in the way that they tax landlords. These changes have, for the most part, all resulted in higher taxes for landlords and reduced after-tax returns for the industry in general. The changes include:

- Maintaining the capital gains tax (CGT) for rented property at 28%, when it was reduced to 18% for other assets ‘to provide an incentive for individuals to invest in companies over property’ (HMRC 2016).

- Introduction of a 3% Stamp Duty Land Tax on purchases of residential property other than principal homes (2016) ‘to try and redress the balance between those who are struggling to buy their first property and those who are able to invest in additional properties’ (HM Treasury 2016).

- Requirement to pay CGT on residential property sales within 30 days of sale (previously payable by those submitting self-assessment tax returns [that is, non-company landlords] up to 22 months post-sale) (in the Finance Act 2019; introduced 2020).

- Withdrawal of tax relief on mortgage interest at the landlord’s marginal rate, and replacement with a 20% tax credit (phased in over four years from 2017).

- Rise in corporation tax from 19% to 25% from 2023, which will affect company landlords only (announced March 2021).

The report by the LSE suggests that these changes do not seem to represent a coherent policy or strategy for the sector, having been introduced piecemeal over a number of years. In fact, they appear to be driven both by a general assumption that rental returns are a passive income and a desire to increase the governments tax take from a politically unpopular cohort.

The Theory of Tax on Housing

Yes, as dull as it may sound, there is a theory underlying the taxation of housing. One that has consensus across much of the developed world. It is important to understand this theory, even in its most basic form, to better understand how the UK’s current tax regime compares to other nations internationally.

Property is an Investment Asset for Tax Purposes

Nearly all developed nations tax housing in line with economic theory, which assumes that houses are assets and should therefore be considered an investment good for tax purposes. Intuitively this makes sense as houses have the ability to generate income and to fluctuate in value. This suggests that houses should be taxed in line with other investment goods such as companies, shares and bonds rather than consumption-based goods like food or hygiene products.

At its core, the taxation of housing focuses on the profitability of holding housing. This involves taxing both the rental income earned on a property and the capital gains it accrues. In most cases, both of these are taxed after costs are accounted for, so that investors are only paying tax on their profits not their revenues. Much of the differentiation between international taxation policies focuses on what are and are not appropriate costs which can be deducted from rents and capital gains before tax must be paid.

Property Tax Regimes Outside of the UK

In the vast majority of countries, rental income is taxed in the same way that business income is – allowing for at least some costs. As you might imagine, there is a significant variation in what different countries consider to be fair business costs, with Western European and Scandinavian countries leaning towards a more progressive and high tax system.

Mortgage Interest is Still Tax Deductible in Some Countries

Most countries consider mortgage interest payments to be fair costs and permit both private and corporate landlords to take the equivalent of mortgage tax relief at their marginal tax rate. English landlords were treated in the same way up until 2015, when the government amended the mortgage tax relief. Individual landlords are now taxed on all of their rental income and receive a flat rate tax credit of 20%, meaning that higher rate taxpayers may find themselves paying income tax even if their properties are unprofitable. The only other countries where individual landlords are not afforded mortgage tax relief are Iceland, the Netherlands and France.

Capital Gains are Taxed Differently in Other Countries

There tends to be more variation in the way countries tax the capital gains of landlords. Currently, in the UK, the first £12,300 of capital gains for individual landlords are tax free as of 2020/2021. After that the rate rises to 28% for private landlords with incomes of more than £50,000 and 18% for landlords earning less. In comparison, landlords operating their properties through a limited company will only need to pay a rate of 19%, irrespective of their income. In comparison:

- Landlords in the United States pay federal long-term capital gains tax upon selling a property, with rates of up to 20%.

- Landlords in France pay both capital gains tax (19%) and social security contributions (17.2%). However, there is full exemption from capital gains tax after 22 years and social security contributions after holding a property for 30 years.

- Landlords in Germany have to pay capital gains tax at their personal income tax rate (varying by income), however properties become exempt if they are held for more than 10 years.

Comparing The UK’s Approach to Property Tax

As you may have guessed by this point, the UK’s current tax regime is far from landlord friendly. The London School of Economics’ report describes the UK as lying at the ungenerous extreme of the international taxation spectrum. Individual landlords find themselves with a limited mortgage tax relief of just 20%, limitations on the tax deductibility of furniture and fittings and capital gains taxes which are both higher than other types of investment and which have to be paid more quickly. On top of this, both individual and company landlords face a supplementary 3% stamp duty when purchasing a property.

Landlords Fear UK’s Continuous Legislation of the Private Rental Sector

For many landlords, the fear is that the current trajectory of more taxation and regulation is set to continue, with corporation tax rising, more pressing EPC requirements and the upcoming amendments to Section 21 notices. The problem is that there is only so much more that the UK’s private rental sector can take. Further increasing the regulatory and tax pressures on landlords, such that they sit even further on the international extreme, could force people out of the market altogether, to the benefit of no one. One can only hope that the government takes a more balanced approach before they enact lasting damage on both individual landlords and the sector as a whole.

References

HM Treasury, 2016. Higher rates of Stamp Duty Land Tax (SDLT) on purchases of additional residential properties: Summary of consultation responses. [Online]

Available at: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/508156/SDLT_summary_of_responses_final_14032016.pdf

HMRC, 2016. Changes to Capital Gains Tax rates. Policy paper. [Online]

Available at: https://www.gov.uk/government/publications/changes-to-capital-gains-tax-rates/changes-to-capital-gains-tax-rates

Scanlon, K., Whitehead, C. & Blanc, F., 2021. Private Landlords and Tax Changes, London: London School of Economics for the National Residential Landlords Association.

Disclaimer: This Landlord Vision blog post is produced for general guidance only, and professional advice should be sought before any decision is made. Nothing in this post should be construed as the giving of advice. Individual circumstances can vary and therefore no responsibility can be accepted by the contributors or the publisher, Landlord Vision Ltd, for any action taken, or any decision made to refrain from action, by any readers of this post. All rights reserved. No part of this post may be reproduced or transmitted in any form or by any means. To the fullest extent permitted by law, the contributors and Landlord Vision do not accept liability for any direct, indirect, special, consequential or other losses or damages of whatsoever kind arising from using this post.