Financial markets are starting to get frothy. Economic headwinds are beginning to churn the waters of global financial markets, with volatility spiking and asset prices tanking over the course of the year. Whilst the causes may be abstract and miles from our shores, their effects have very real consequences for homeowners and landlords throughout the United Kingdom.

The Bank of England’s base rate has risen dramatically since the start of the year, pushing mortgage rates up from their historic lows. Despite this, financial markets expect that interest rates will continue to rise substantially over the coming 12 months and, in doing so, continue to push mortgage rates even higher. A significant portion of homeowners and landlords on variable rates, or with fixed rates soon to expire, are about to see their monthly mortgage payments rise exponentially. In turn, this may have devastating effects on house prices and the housing market in general.

What is Causing Mortgage Rates to Rise?

On Thursday the 22nd of September, the Bank of England raised rates by 50 basis points (0.5 percent), to their current level of 2.25 percent. The following day, the government announced a fiscally expansionary budget, considerably increasing the government’s anticipated borrowing requirements over the coming years. Simultaneously, global financial markets continued to sell off, driven by a deteriorating economic outlook and aggressive Federal Reserve rate hikes. The consequence being that Sterling and Gilts (UK government debt) sold off, with the value of pound sterling falling to its lowest level versus the dollar since 1971 – although it has since recouped some of its losses.

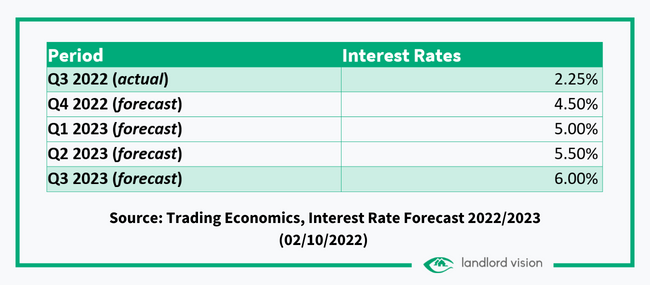

Of more worry is what financial markets expect to happen in the near future. Markets believe that inflation will remain elevated over the coming months, with gas prices continuing to push up household heating bills and the cost of production. This will coincide with slowing economic growth and a deterioration in government borrowing requirements. As such, markets are pricing in the prospect that the Bank of England will need to increase its base rate to 6 percent by this time next year.

The Relationship Between the Base Rate and Mortgage Rates

The ‘Base Rate’ is the interest rate that the Bank of England sets when lending to other banks. In a very simple sense, it is an indication of the cost that high street banks pay when they themselves borrow money. As banks are in the business of making more money, they typically lend to households and landlords at a rate which is above that of the base rate. The difference between the base rate and the mortgage rate that a bank may charge when lending, is a reflection of their need to make a profit on the loans they provide and the risk premia that they attach to lending to you. The riskier the loan, the higher the rate.

When the base rate rises, banks usually respond by increasing the interest rates that they apply to their own loans. Equally, banks may increase the rates they charge in expectation of the base rate rising if they believe this is likely to happen.

What Do Rising Interest Rates Mean for Landlords?

As already established, a rising Bank of England base rate means mortgage rates are likely to rise. This is already apparent, with many lenders charging as much as 4 percent for a 2-year fixed rate mortgage, compared to between 1-2 percent this time last year. Landlords and homeowners on tracker rates and standard variable rates (SVR’s), will have already seen their monthly repayments increase substantially, whilst it is estimated that an additional 2.1 million fixed-rate mortgage deals will expire between now and the end of 2023.

The monthly repayments on a typical £150,000 mortgage could leap by as much as £500 per month or £6,000 per year. For borrowers with more than £200,000 in outstanding mortgages, monthly payments could jump by more than £724 per month. That is a staggering additional £8,688 or more in mortgage payments over the course of a year. Alice Guy, of the Mail on Sunday, estimates that households on fixed rate mortgages could pay £13 billion extra per year in mortgage costs if interest rates hit 6 percent in 2023.

The rise in interest rates will impact landlords especially. Whilst 54 percent of homeowners own their homes outright, landlords are more likely to rely on leverage (borrowing) to finance the purchase of properties and turbo-charge their returns. This means that landlords who have not locked in long-term fixed rate mortgages could see their borrowing costs spiral across their portfolios, at a time when the profitability of buy-to-lets has already been hammered by punitive government legislation.

Banks responded to the market turmoil last week by withdrawing more than 1,000 mortgage deals which were deemed uneconomical last week, according to Moneyfacts. There are around 850 buy-to-let mortgages available to landlords currently, with an average rate of 5.26 percent for a five-year fixed rate deal. In comparison, landlords could have refinanced on a similar deal at just 3.25 percent in August.

Some industry experts are calling for landlords to ‘stay calm’ in the face of rising interest rates. Chris Norris, Director of Policy & Campaigns at the NRLA suggests that landlords should: “keep calm. No one is sure what is going to happen but take this opportunity to consider your future plans. Those with three months or less left on a fixed-rate deal might start looking around right now as lenders can sign up new landlords to a future deal that begins in a few months time”.

Equally, Lee Grandin, owner of buy-to-let broker Landlord Mortgages, highlights that “… there is still a shortage of properties available for people to rent in major cities, such as London. So, if mortgage rates rise you should perhaps consider raising the rent rather than simply selling up”. Although, it has to be caveated that tenants are facing their own cost of living increases. In some cases, it may not be prudent or, in some cases, ethical, to dramatically increase rents.

The Impact on the UK Housing Market

Rising mortgage rates themselves will prove to be a substantial headwind for landlords, but the impact they may have on house prices should be of equal concern. Rising mortgage payments could well bring about a housing market crash, with property prices plummeting. A substantial number of households and landlords will struggle to meet their obligations if mortgage payments increase by £500-£700 per month. The basic financial viability of renting out properties may be called into question unless the rate increases can be passed onto tenants to some degree. Otherwise, people will be forced to sell up.

House prices for the 12 months to July were up 15.5 percent and averaged £292,000, according to the Office for National Statistics. Analysis conducted by Oxford Economics suggests that houses are overvalued by as much as 30 percent, indicating that a ‘scenario whereby house prices crash is looking increasingly likely’. It is feared that forced selling, by landlords and homeowners unable to meet their mortgage payments, will trigger a general market crash in property prices, with some commentators questioning whether prices could fall as much as 20 percent over the coming year.

Analysts at Credit Suisse suggest that, if interest rates reach 6 percent next year, house prices could fall as much as 15 percent. Andrew Garthwaite of Credit Suisse states that: “On current swap rates, the average mortgage will be 6.3 percent. House prices could easily fall 10 to 15 percent”. This is a view shared by Andrew Wishart, senior property economist at Capital Economics, who warns: “The rise in market interest rates that has already happened will push up mortgage rates to at least 6 percent and reduce the size of loans that lenders can offer. The resulting drop in buying power makes a significant drop in house prices inevitable. At the current level of house prices, an increase in mortgage rates to 6.6 percent would cause the cost of repayments on a new mortgage to rise to their highest level since 1990.”

Is it Time to Batten Down the Hatches?

It’s without a doubt that landlords are in for a tough ride over the next twelve months. However, things can’t always be plain sailing. Part of investing and part of being a landlord is surviving the tough times, as well as the periods when the sun is shining. In the short run, things may become more difficult, however as time progresses the market will adjust, and new opportunities will arise.

In the meantime, landlords should consider building up their cash reserves as protection. It always helps to stay liquid and have a rainy day fund, should the cost of living crisis increase lead to increased voids. At the same time, any landlords who are on variable rates or have fixed terms expiring should consider locking in a fixed rate mortgage whilst they can. Although there is no guarantee that mortgage rates will rise as much as is forecast, landlords should ask themselves whether they can continue to afford to own their properties if they do.

Landlords should also take the time to work out the appropriate amount to raise rents by. This is always a difficult subject, with no correct answer. But with interest rates rising dramatically and inflation in the double digits, rents must also rise to some degree. Whether it is fair to raise rents in line with inflation depends on the property, location, and current tenant situations. However, landlords will no doubt be expected to shoulder a fair portion of the increase in costs.

Finally, it remains important to keep your eyes on the future for when the tides eventually turn. When the market begins to settle and things begin to look more positive, there will be numerous opportunities out there for landlords. There will be a significant number of properties selling at a discount, with attractive yields and long-term growth potential. If you can manage to weather the next 12 months, it may well set you up to benefit for the next decade.

References

Luke Barr, Financial Mail on Sunday. 2022. Homeowners set for £13bn hammer blow: Millions face rocketing bills for mortgages as base rate tipped to reach 6%. www.thisismoney.co.uk. [Online] 1 October 2022. https://www.thisismoney.co.uk/money/markets/article-11269681/Millions-face-rocketing-mortgages-bills-base-rate-tipped-reach-6.html?mrn_rm=rta.

The Financial Times. 2022. Where this UK mortgage meltdown will really bite. www.ft.com. [Online] 28 September 2022. https://www.ft.com/content/1795e739-6e11-43cd-bf92-d7d2ad0324b2.

Toby Walne, Financial Mail on Sunday. 2022 . ‘I must sell or gamble I can weather the storm’: Stay calm, plea to landlords as buy-to-let loan deals disappear. www.thisismoney.co.uk. [Online] 1 October 2022 . https://www.thisismoney.co.uk/money/mortgageshome/article-11269617/Stay-calm-plea-landlords-buy-let-loan-deals-disappear.html.

Trading Economics. 2022. Interest Rate Forecast 2022/2023. Trading Economics. [Online] 2 October 2022. https://tradingeconomics.com/forecast/interest-rate?continent=europe.

Zoopla. 2021. Revealed: how long it’s taking buyers to complete in 2021. [Online] 04 February 2021. https://www.zoopla.co.uk/discover/property-news/average-time-for-a-sale-to-complete/.