Fred Harrison’s 18-Year Cycle has captivated a large proportion of the property investment community. New posts and publications on the topic are released on a seemingly daily basis, as the theory continues to gain ground.

For those of you wondering ‘what exactly is the 18-Year Cycle?’, it may be worth reading our post introducing the concept:

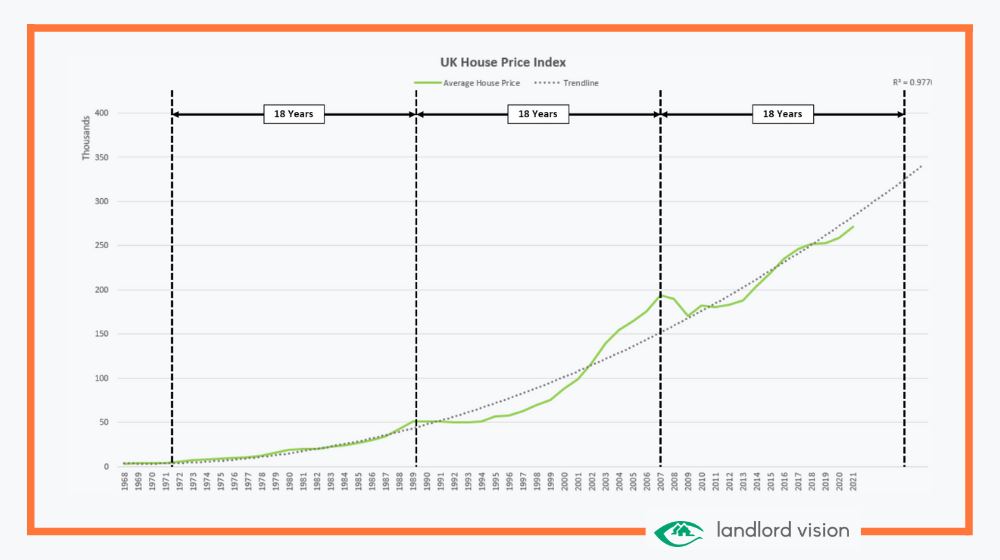

Harrison first introduced the 18-Year Cycle so far back as January 1999, accurately predicting the global housing crash and the subsequent financial crisis which it spurred. One of the reasons the theory has become so popular is that, even to this day, the market appears to be performing in line with the 18-Year Cycle.

Given that the last property market crash occurred in 2007, the theory suggests that the UK property market entered its final ‘Boom’ phase in 2020. As many of you will already be aware, house prices increased by 8.5% throughout 2020, further adding credibility to Harrison’s theory. However, whilst the current boom in prices coincides with the theory, one of the key driving factors has been a worldwide global pandemic, the like of which has not been seen in over 100 years. This poses the question of whether the pandemic has influenced the 18-Year Cycle and what it’s effects may be.

Can The 18 Year Cycle Be Broken?

One of the most seductive features of the 18-Year Cycle is that it is predicated on over 200 years of UK house price data, ranging all the way back to 1776. This affords Harrison’s theory an unmatched empiricism, based upon 14 successive 18-Year Cycles. However, history also demonstrates the exceptions to the rule.

Whilst Harrison has been able to trace 200 years of successive 18-Year Cycles, both 1920 and 1938 proved to be exceptions to the pattern. Theory would suggest that both of these years should have witnessed a crash, with house prices falling significantly. However, the impact of both the first and second world war helped to deflect the traditional cycle. The colossal combination of world-wide destruction and unprecedented government spending acted as a countervailing economic weight, offsetting the impending crash in house prices. Harrison likens the world wars to dynamite being thrown down an oil-well which is already aflame: the blast destroys the fire. In this case, the immense upheaval of war broke the cycle.

Could The Pandemic Be Like Dynamite for the 18 Year Cycle?

The recent Coronavirus pandemic shares a number of similarities with the first and second world war. Instead of destroyed factories and conscripted workforces, the pandemic closed businesses and confined workers to their homes. In the same way in which wars forced production to shift from consumer goods to focus on munitions, the pandemic prioritised PPE and vaccines ahead of hospitality and consumerism. Equally, both the wars and the pandemic have necessitated tidal waves of government expenditure, as the state sought to dictate the economic needs of the nation.

Given their similarities, it wouldn’t be unfair to suggest that the pandemic could impact the property cycle in a similar manner to the first and second world wars. As was the case in 1920 and 1938, the impending crash could be deflected and postponed. However, this thinking perhaps overstates the repercussions of the pandemic. The world wars lasted 4-6 years and required decades of rebuilding to repair the economic, social and populational scars that they caused. The rationing of food in the UK continued for nearly a decade after the end of the second world war. It is unlikely that the direct effects of the pandemic will continue to the same degree.

Therefore, whilst the recent pandemic does share some short-term similarities with the world wars, it is unlikely that it has sufficient dynamite to fully extinguish the flame of the current 18-Year Cycle. That being said, the pandemic may still influence the cycle in a less severe manner. As the government unwinds its expenditure and the economy re-adjusts, the current boom phase may lose some of its momentum. This may slow the boom, but it is unlikely to arrest the long-term increase in house prices that the 18-Year Cycle predicts.

What Does Harrison Say About the Pandemic?

Interestingly, Harrison discussed the topic of the pandemic in a recent interview published on the website This Is Money. During the interview, Harrison highlighted that he had seriously considered whether the pandemic had the potential to delay the boom phase of the cycle. However, the continuing evidence of house price growth has only reinforced his view that the virus does not have the power to stall the cycle.

Harrison said: “I concluded that the 2020s would be a re-run of the years after the flu pandemic of 1918, which terminated with the Crash of 1929. There might be a short-term easing off, as the post-pandemic world returns to something akin to normal, but the price trend will continue upwards.”

What Are Harrison’s Predictions for The Current Cycle?

As the pandemic is unlikely to have caused any significant disruption to the current 18-Year Cycle, Harrison continues to predict a market crash in 2026:

“Each 18-year cycle has a mid-cycle downturn, For the current cycle, that was 2019 and sure enough, there was an on-time downturn. The overall trend from here is up and up – squeezing peoples purchasing power till the music stops in 2026. House prices will peak in 2026 followed by a recession that will eclipse what happened in 2008. Then, everyone will be shocked, and people will wonder why they were not warned”, explains Harrison.

For Harrison, the boom-and-bust nature of house prices are an inextricable feature of the housing market itself: “This trend is built into the DNA of the financial model, which is treated as sacrosanct. Young people will continue to be squeezed out of the housing market. The capital gains will continue to roll in until once again, the merry-go-round comes to an abrupt halt.”

Harrison highlights that the ingredients for a housing crash are the same as they have always been: ‘When prices become insupportable, with disposable incomes crushed by mortgage liabilities, people retract on consumption; as the housing market freezes, enterprises find the demand for their goods and services beginning to disappear, and hey presto, we have a recession.”

What Does This Mean for Landlords?

Whilst it is certainly an alluring theory, the 18-Year Cycle is by no means gospel. Many have tried and failed to predict both financial and housing markets. However, whether or not you believe in the predictive power of the 18-Year Cycle, it does appear that the market will continue to follow its trajectory in the short-term.

Market manias appear to be entwined into the psyche of our nature. So long as there has been markets, there have been speculators seeking a quick return, be it tulips, gold, bitcoin or property. More likely than not, the strong performance of house prices will only encourage further speculative purchases, further feeding the cycle of ever higher prices – much as Harrison predicts. It could well be that we are set for more years of booming growth.

However, with the predictions of growth come the looming spectre of a crash. If prices do begin to spiral out of control, the Bank of England may need to step in. Lines of credit may begin to tighten and borrowing costs may rise. How many properties will continue to be profitable if mortgage rates return to 5-6%? Speculative investors who believe in the merits of the 18-Year Cycle may want to take the coming months as an opportunity to add to their portfolio during the early stages of a boom, though prudent investors may also want to ensure that they retain sufficient cash buffers whilst doing so.

Disclaimer: This ‘Landlord Vision’ blog post is produced for general guidance only, and professional advice should be sought before any decision is made. Nothing in this post should be construed as the giving of advice. Individual circumstances can vary and therefore no responsibility can be accepted by the contributors or the publisher, Landlord Vision Ltd, for any action taken, or any decision made to refrain from action, by any readers of this post. All rights reserved. No part of this post may be reproduced or transmitted in any form or by any means. To the fullest extent permitted by law, the contributors and Landlord Vision do not accept liability for any direct, indirect, special, consequential or other losses or damages of whatsoever kind arising from using this post.