In this post, we will look at when it is beneficial to use a company to grow a property portfolio.

Using a Company to Grow Your Property Portfolio

A company comes into its own when the plan is to reinvest the rental profits in more property, rather than to draw them out for living expenses.

Jane has a well-paid job, and pays Income Tax at 40%.

She wants to build up a portfolio of residential properties, using the profits from the rentals to fund the acquisition of other properties.

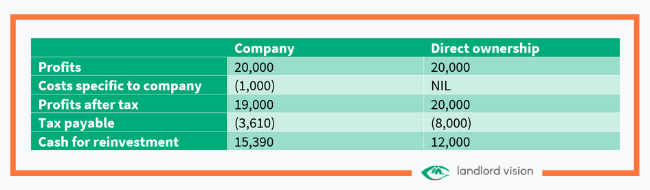

She begins with a portfolio of 10 buy to let properties in 2020, but instead of taking the profits out of the company, she leaves them there to fund the deposits on new properties.

In the first year, the position will be:

If the pattern is repeated in the following years, it is clear that she will be able to spend more money (within the company) on investing in new properties than she would if she were paying Income Tax on the rents. This relative saving will result in a “virtuous cycle”, whereby each year can result in better and better results, thanks to the lower Corporate Tax rate.

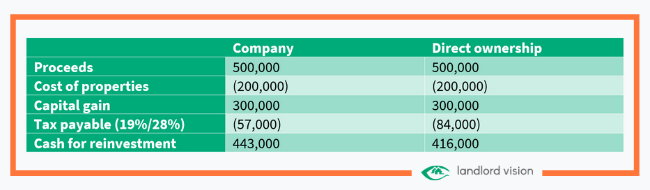

In (say) 2030, Jane’s company sells some of its properties. The disposals are subject to Corporation Tax on capital gains:

The company benefits from a significantly lower tax rate than Jane would pay on residential property that she owned personally. The net result is that the company pays a lot less tax than Jane would, if she owned the properties personally. (We are assuming in the CGT calculation that Jane has already used her Annual Exemption).

Note: Jane would normally have to pay more tax to access those funds in the company – the so-called “double tax charge” – where the company pays tax on profits or gains, and then the shareholder/director pays tax to get the funds out of the company for personal use.

But these examples serve to illustrate how companies have the advantage if they are able to retain their profits, year on year, to boost growth. This will normally apply only if a landlord or landlady has sufficient other income or wealth – or a portfolio of sufficient size – that he or she can afford to the leave most profits (if not all) in the company wrapper.

However, there is a recent development that will, for many residential landlords, tip the balance strongly in favour of incorporation, whether they keep the profits in the company or not. That is the disallowance of finance costs in relation to the letting of residential property.